Markets and Economy: Under New Management

by Tim Doyle, Chief Investment Officer, CFP®, MBA

The 2026 Major League Baseball season began in late March and, heading into this year, I had reasonably high hopes for my Philadelphia Phillies given their strong starting lineup and solid pitching staff. In fact, in mid-March, my wife and I took our two boys to Phillies spring training in Clearwater, Florida to watch a few pre-season games and get our boys a closer look at some of their favorite players. At the time, we had optimistic visions of another National League East title and a deep playoff run that would culminate with a trip to the World Series.

Well, fast forward a few short weeks into the season, and the Phils had an MLB-worst 9-19 record and capped the disappointing start by firing the team’s manager, Rob “Topper” Thompson at the end of April. That was not the start Phillies fans were hoping for, to say the least. In professional sports, I’ve always been fascinated by a team’s decision to make changes at the coach/manager level, particularly in-season. Is there really much a new manager can do to change the trajectory of a struggling team? After all, as the saying goes “it’s not the X’s and O’s, it’s the Jimmy’s and the Joe’s.” Sure, the manager can have an impact, but outcomes are largely going to be determined by player performance and a litany of other uncontrollable factors.

When considering the U.S. economy, investors are about to experience a managerial change, of sorts, as the Senate recently confirmed Kevin Warsh as Federal Reserve Chairman on May 13th. Warsh succeeds Jerome Powell, who will serve as a Fed governor and remain a voting member of the Federal Open Market Committee (FOMC) until his term ends in early 2028.

The key question in the minds of many investors is, “will anything materially change now that Warsh is at the helm of the Fed?” After all, I’m already seeing articles in financial media detailing how Kevin Warsh’s tenure as Fed Chairman may impact the stock market, the bond market, mortgages, auto loans, student debt, and more. So, in this month’s investor letter, we’ll begin by outlining what we expect from a Federal Reserve with Kevin Warsh at the helm along with some of the challenges he faces in the weeks and months ahead.

An Unenviable Job

Kevin Warsh is set to lead his first FOMC meeting in mid-June and, as Simpsons character Ned Flanders would say, he finds himself “in a dilly of a pickle.” As many of us know by now, the Federal Reserve has a dual mandate to set monetary policy that supports both full employment and stable prices. Right now, Warsh and the FOMC face challenges in meeting both of those mandates as cracks have emerged in the labor market and inflation has surged considerably in recent months.

In fact, on May 12th, the April Consumer Price Index (CPI) report was released and showed that Headline CPI (which includes food & energy) rose an eye popping 3.8% year-over-year – the highest reading since May of 2023. That is a meaningful step in the wrong direction after inflation trended closer to the Federal Reserve’s 2% target in 2024 and 2025.

Consumers then received a double-whammy as the April Produce Price Index (PPI) report was released the following day on May 13th. PPI tracks prices at the wholesale and manufacturing level before goods reach consumers, and the April PPI report showed that producer prices rose a hefty 6.0% year-over-year. This represents the highest PPI reading since December of 2022. Producer prices often function as a leading indicator of what may eventually show up in consumer prices, so a reading of 6% for PPI certainly caught the eye of many economists and analysts who were predicting PPI closer to 4.9% year-over-year.

When reviewing key contributors to inflation, the chart below helps to illustrate which elements of CPI are pushing aggregate prices higher.

Source: JP Morgan Asset Management – Guide to the Markets

Clearly, the war in Iran and continued closure of the Strait of Hormuz are causing a surge in energy prices as, as-of this writing, Brent Crude Oil prices have risen to nearly $110 per barrel and the national average price per gallon of regular unleaded gas sits at $4.58 according to AAA. As we all know, oil and gas remain the lifeblood of the global economy and, if there is no resolution that re-opens the Strait of Hormuz in the near future, higher energy prices are bound to bleed into other elements of inflation like Core Goods.

Furthermore, as we reviewed in last month’s letter, nearly one-third of the world’s fertilizer supply is tied to the Strait of Hormuz. So, there will likely be upward pressure on food prices in the weeks and months ahead as higher fertilizer prices are passed-on to consumers and/or there is a lower crop yield due to lack of fertilizer which reduces overall supply. The graph below from the American Farm Bureau Federation helps to show which crops may be most impacted as farmers are unable to afford all required fertilizer to produce their desired yields.

This brings us back to Kevin Warsh and his new role as Fed Chairman. Historically speaking, Kevin Warsh had been known as a bit of an ‘inflation hawk’, as we say in the world of economics and investing. This means that he’s traditionally been in favor of raising interest rates in order to aggressively squelch inflation, particularly in his early days as a Fed Governor in the mid-2000’s.

However, in recent years, Kevin Warsh has been more open to cutting interest rates, which is the fervent desire of the man who appointed him as Fed Chairman – President Donald Trump. Trump has been very vocal about the fact that he’d like to see the fed funds rate lowered, and he’s often been publicly critical of Jerome Powell for the FOMC’s unwillingness to do so.

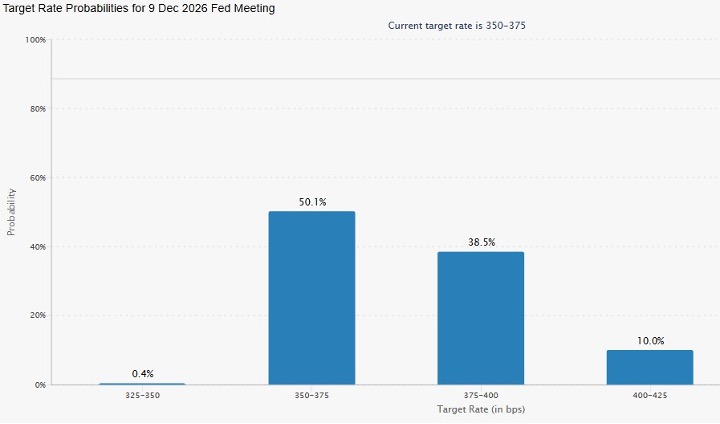

So, will President Trump’s wish for lower interest rates come true? In my opinion, it’s highly unlikely. There is simply no justification for cutting interest rates in this inflationary environment, and I am not alone in that assessment. The chart below helps to illustrate this by showing probabilities for what the fed funds rate will be at year-end. According to fed fund futures markets, investors are currently assigning a 50% probability that interest rates will remain unchanged (3.50%-3.75%). However, what’s more eye-opening is the fact that nearly 39% of investors are actually betting that interest rates will RISE another 0.25% between now and year-end.

Source: CME Group Fedwatch Tool

Long story short, investors believe that it’s much more likely that the Fed will raise interest rates versus lowering them, and this would hardly be the outcome President Trump is looking for. Again, Kevin Warsh will soon be in the unenviable position of leading the Fed as they navigate a weakening labor market and rising inflation – all while likely facing political pressure to ease monetary policy through lowering interest rates.

The Investor / Consumer Dichotomy

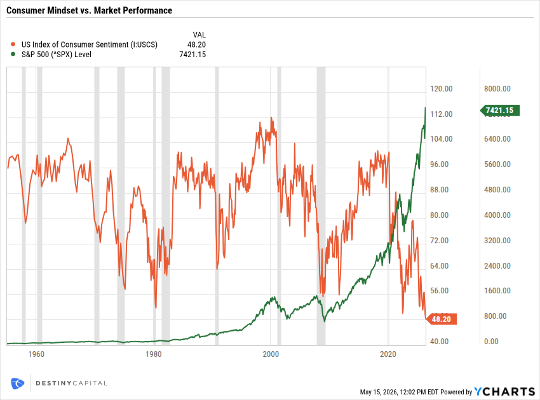

I’ve written this many times in previous letters, but one key lesson I took from 2022 is to realize how damaging elevated inflation can be to the consumer mindset. As aggregate prices rise, consumers grow increasingly pessimistic. That continues to be the case in 2026 as consumer sentiment has fallen to an all-time low of 48.2 as headline inflation has moved closer to 4%. Yet, the stock market – as measured by the S&P 500 – continues to reach new all-time highs in recent days and weeks, and we now have the largest-ever gap between overall consumer sentiment and stock market performance, as you can see in the chart below.

It’s somewhat fascinating to see how there can be such rampant pessimism among consumers while investors remain relatively exuberant. As is usual, economic reality probably lies somewhere in between these two extremes. Regardless, U.S. corporations continue to give investors reasons to be optimistic as Q2 2026 earnings season comes to a close.

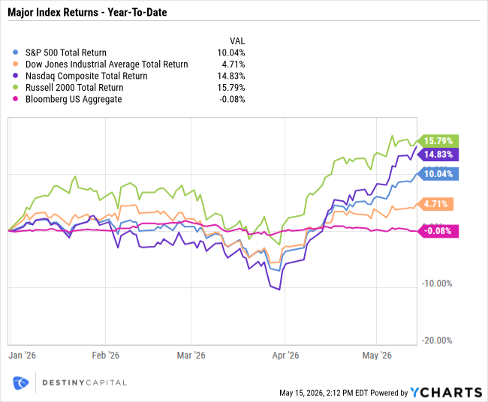

With just over 90% of S&P 500 companies reporting, earnings figures have been nothing short of incredible. To date, 84% of these companies have beaten earnings estimates while 80% have reported a positive revenue surprise. These numbers are well above the 5 and 10 year averages for both earnings and revenue beats.

Investors have also seen incredible year-over-year growth in both revenues and earnings. Revenue growth has reached 11.4% – the highest level since Q2 of 2022 while earnings growth has reached a staggering 27.7% year-over-year. If this earnings growth figure holds, it would be nearly 15% higher than the earnings growth estimate heading into Q2 and would also mark the highest earnings growth rate since Q4 of 2021. As we’ve written many times, earnings growth is the key driver of long-term shareholder value, so these figures are encouraging and it’s not much of a surprise that markets have reacted positively, as seen in the chart below that shows year-to-date returns for the major U.S. stock and bond market indexes.

Moving forward, much is still dependent on the outcome of the war in Iran and whether or not the Strait of Hormuz is opened in a timely fashion. The longer the Strait remains closed, the longer the inflationary effects are likely to linger. Given the relationship between high inflation and consumer pessimism, it is likely that political pressure will build demanding a resolution in Iran as the U.S. approaches mid-term elections.

Ultimately, while leadership at the Fed may change, the constraints of the current environment have not. Much like a new manager stepping into a struggling clubhouse, Kevin Warsh inherits conditions that will dictate outcomes far more than philosophy alone. For investors, staying disciplined and focused on fundamentals—not headlines—remains the most reliable path forward. As always, if you have any questions, please don’t hesitate to submit them to my CIO Mailbag or please reach out to your Destiny Capital team with anything you need.

Important note and disclosure: This article is intended to be informational in nature; it should not be used as the basis for investment decisions. You should seek the advice of an investment professional who understands your particular situation before making any decisions. Investments are subject to risks, including loss of principal. Past returns are not indicative of future results. Advisory services offered through Destiny Capital Corporation, an Investment Adviser registered with the U.S. Securities & Exchange Commission.

2024 YCharts, Inc. All Rights Reserved. YCharts, Inc. (“YCharts’) is not registered with the U.S. Securities and Exchange Commission (or with the securities regulatory authority or body of any state or any other jurisdiction) as an investment adviser, broker-dealer or in any other capacity, and does not purport to provide investment advice or make investment recommendations. This report has been generated using data manually input by the creator of this report combined with data and calculations from YCharts.com and is intended solely to assist you or your investment or other adviser(s) in conducting investment research. You should not construe this report as an offer to buy or sell, as a solicitation of an offer to buy or see, or as a recommendation to buy, sell, hold or trade, any security or other financial instrument. THE IMPORTANT DISCLOSURES FOUND AT THE END OF THIS REPORT (WHICH INCLUDE DEFINITIONS OF CERTAIN TERMS USED IN THIS REPORT) ARE AN INTEGRAL PART OF THIS REPORT AND MUST BE READ IN CONJUNCTION WITH YOUR REVIEW OF THIS REPORT. Disclosure – YCharts

Share this

Stay Ahead with Smart Investments

Learn how to invest wisely and minimize risks to protect your retirement savings.

Achieve Your Retirement Goals

Get personalized advice to meet your retirement goals. Book your call with Destiny Capital now.