From Mag Seven to Lag Seven – Are Tech Titans Turning Mortal?

by Tim Doyle, Chief Investment Officer, CFP®, MBA

As a father, I’ve had a bit of an eye opening introduction to youth sports with my two boys over the past few years. Years ago, I recall taking my oldest son to his first baseball lessons around age six at a local sports complex. Upon signup, it appeared to be a low key camp where a group of kids met with coaches once a week for an hour to learn some of the basics of throwing, catching, fielding, and hitting. My son and I pulled up to the complex for his first day of lessons, and we moseyed in carrying his water, glove and helmet in an old reusable shopping bag as I held his little $20 tee ball bat from Target.

You’ll then imagine my surprise when, as all of the kids were getting settled, I glanced around the room to see that every single other boy had a fancy baseball backpack with at least two baseball bats attached to each side. Many also had colorful arm sleeves, batting gloves, and other shiny new gear. I hesitated for a moment and wondered if we were in the right lesson as – based on appearances alone – it seemed like we had walked into a room of elite travel ball prodigies. Alas, as training commenced, it became quickly apparent that the majority of the kids could barely catch or throw, despite the $500 of gear they carried on their backs into the complex that day.

When I played little league baseball as a kid, we had one ‘team bat’ that looked like it was forged alongside cannonballs during the revolutionary war, and we all shared a ‘team helmet’ that wobbled on our heads as we walked to the plate. So, it’s been an adjustment to see just how much money parents can spend on gear – particularly in a sport like baseball. Is that $350 Easton Hype Fire two piece composite bat really going to help your kid hit better than the $30 aluminum Rawlings bat you can pick up at WalMart? Maybe, but probably not – at least in the early years of youth baseball. However, as a parent and if you have the financial resources, it can be hard not to fall into that spending trap. You see everyone else doing it, but you also come to the realization that you’ll eventually have to see a return on investment for all that spending.

Investors are coming to a similar realization here in 2026 as we’ve seen a handful of the lauded ‘Magnificent Seven’ stocks (Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA, and Tesla) struggle this year. Many of these stocks are considered to be “AI Hyperscalers” – the companies spending extraordinary sums of money on the buildout of AI infrastructure. In my 2026 preview at the end of last year, I openly wondered if and when investors would begin to demand some kind of tangible benefit tied to all of this rampant AI spending. So, in this month’s letter, we’ll focus on these mega cap AI hyperscalers to gauge whether or not investors are seeing enough of a return on investment for all of this AI capex (capital expenditure) and how it has impacted the stock market as overall.

By the Numbers

As we surpass the halfway mark of 2026, the S&P 500 index is up roughly 9% as-of this writing. That sounds like a very healthy return, and it absolutely is. But as you look beyond the headline numbers, the story gets a bit more nuanced. Over the past few years, and as many of you know, the Magnificent Seven stocks have largely driven the strong performance of the entire S&P 500. However, that dynamic has shifted here in 2026, as the S&P 493 (all other stocks not in the Mag 7) is up +13% while the Mag 7 stocks are up only +3% on an equal weight basis.

That shift is worth noting as, in 2023 through 2025, the Mag 7 stocks accounted for 63%, 55%, and 46% of the S&P 500’s return in each consecutive year. Meanwhile, in 2026, the Mag 7 stocks accounted for only 12% of the S&P 500’s return, as you can see in the chart below. In short – instead of driving the stock market, these stocks are dragging the market.

Why – Enablers vs. Implementers

To explain what is happening, I find it helpful to divide the AI investing world into two basic groups. I tend to refer to these groups as the enablers and the implementers.

The enablers are the companies that make the physical infrastructure behind AI. They design the chips, they manufacture them, they make the networking equipment that connects them, and they build the tools that other companies need to run large-scale AI systems. Companies like Nvidia, Advanced Micro Devices, Broadcom, Micron and their peers all sit in this camp. When a Mag 7 company (or anyone else) spends a dollar on AI, some meaningful piece of that dollar ends up as revenue for an enabler.

The implementers are the companies making the big bet – they are the ones spending the money on the AI infrastructure and hoping to translate that spending into new products, new services, and new profits down the road. NVIDIA aside, this is where most of the Magnificent Seven now sit. Microsoft, Alphabet, Amazon, and Meta are collectively expected to spend somewhere in the neighborhood of $725 to $760 billion on AI-related capital expenditure in 2026 alone. That is not a decade of spending. That is just one calendar year.

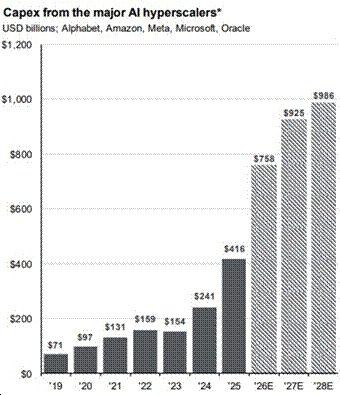

The chart below helps to illustrate the staggering pace of capex spending growth from these AI hyperscalers. In 2019, this group of companies spent about $71 billion combined on AI buildout. In 2025, that total rose to roughly $416 billion. This year, AI capex is expected to rise to $760 billion and – based on current guidance – the number could climb to over $900 billion in 2027 and approach $1 trillion by 2028.

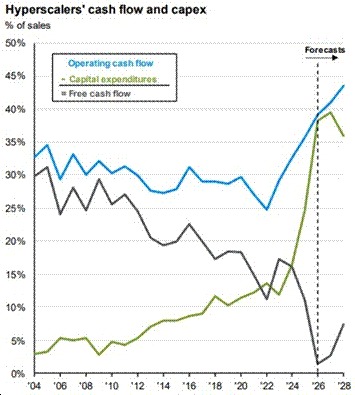

This spending has had a meaningful impact on the financials of each of these companies. For example, Meta’s free cash flow, which was $26 billion in the first quarter of 2025, fell to $1.2 billion in the first quarter of 2026. Morgan Stanley now expects Amazon to run negative free cash flow of about $17 billion for the full year. Think about that for a second. Amazon – a company generating hundreds of billions in revenue – is expected to spend more than it earns because the AI buildout is deemed too important to slow down. Microsoft’s operating margins hit a three-year low in its most recent quarter as its data-center spending outpaced revenue growth from AI.

The chart below helps to show how free cash flows (grey line) of the AI hyperscalers have eroded as capex spending has increased substantially since around 2023.

The Market is Demanding Progress

The market’s recent reaction to AI spending, in my view, is not a rejection of AI as a technology or as a long-term investment theme. It is a rejection of open-ended checkbook writing without a clear line back to earnings.

You can see how investor mindset has shifted in the way the market has reacted to earnings this year. When certain implementers reported first-quarter results, several of them beat consensus earnings estimates by wide margins. In fact, the Magnificent Seven as a group grew earnings more than 50 percent year-over-year, and yet many of their stocks sold off on the announcements and subsequent forward guidance from company executives. Meta fell nearly 9 percent the day after earnings because the company raised forward guidance on AI spending. Microsoft stock slipped even though it beat across the board because margins compressed.

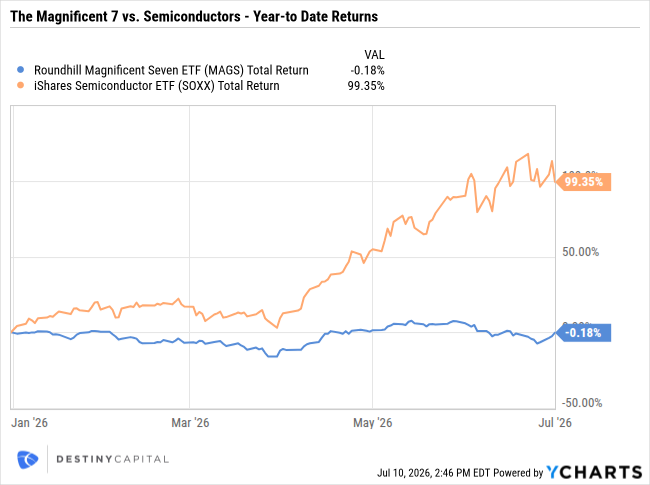

Meanwhile, the enablers – the chipmakers and memory producers who are, quite literally, on the receiving end of all that spending – have been rewarded with the kind of gains chip stocks last saw in 1999. You can see this dynamic illustrated in the chart below that shows the year-to-date returns of the iShares Semiconductor ETF (SOXX) versus the Magnificent Seven ETF (MAGS) which shows semiconductors up 99% while the Mag 7 ETF remains flat-to-negative.

A little history helps to add some perspective here. In 1999, the fiber-optic and telecom-equipment companies – the enablers of the internet – had a spectacular year as everyone was building the physical infrastructure of the web. The implementers buying all of that gear did well for a while too, but by 2001 and 2002 markets started asking who was actually going to earn a profit on the buildout. Clearly, there were some winners (think: Amazon, Alphabet, Oracle, etc.), but also a fair share of losers.

This is not a prediction that the Magnificent Seven are heading for a dot-com-style collapse. Their businesses are far larger, far more profitable, and far more diversified than the average 1999 company. Nvidia alone earned more in the last twelve months than the entire fiber-optic sector did in its best year. This is a much healthier setup across the board and each of these companies operate on a much stronger foundation. But the pattern of markets rewarding the enablers first and eventually demanding proof and justification from the implementers is a familiar one, and it is a useful lens to view what we are seeing now.

A Brief Note On Earnings

As we enter the beginning of earnings season, the S&P 500 is expected to grow earnings a staggering 23% year-over-year in the second quarter according to FactSet. If true, that would be the second consecutive quarter of growth above 20 percent, and the seventh consecutive quarter of double-digit earnings growth. Furthermore, revenue growth is expected to come in above 10%, while net profit margins for the S&P 500 are expected to hit 12.9%, which is close to a record high. On its face, this is one of the strongest earnings backdrops of the last decade.

However, while these headline earnings numbers are important, investors will be listening not just for what the enablers are earning, but for what the implementers are saying about the return on investment they are getting on AI spending. Therefore, forward guidance, capex commentary, and margin trajectory may matter more than the headline beats in the weeks ahead.

Important note and disclosure: This article is intended to be informational in nature; it should not be used as the basis for investment decisions. You should seek the advice of an investment professional who understands your particular situation before making any decisions. Investments are subject to risks, including loss of principal. Past returns are not indicative of future results. Advisory services offered through Destiny Capital Corporation, an Investment Adviser registered with the U.S. Securities & Exchange Commission.

2024 YCharts, Inc. All Rights Reserved. YCharts, Inc. (“YCharts’) is not registered with the U.S. Securities and Exchange Commission (or with the securities regulatory authority or body of any state or any other jurisdiction) as an investment adviser, broker-dealer or in any other capacity, and does not purport to provide investment advice or make investment recommendations. This report has been generated using data manually input by the creator of this report combined with data and calculations from YCharts.com and is intended solely to assist you or your investment or other adviser(s) in conducting investment research. You should not construe this report as an offer to buy or sell, as a solicitation of an offer to buy or see, or as a recommendation to buy, sell, hold or trade, any security or other financial instrument. THE IMPORTANT DISCLOSURES FOUND AT THE END OF THIS REPORT (WHICH INCLUDE DEFINITIONS OF CERTAIN TERMS USED IN THIS REPORT) ARE AN INTEGRAL PART OF THIS REPORT AND MUST BE READ IN CONJUNCTION WITH YOUR REVIEW OF THIS REPORT. Disclosure – YCharts

Share this

Stay Ahead with Smart Investments

Learn how to invest wisely and minimize risks to protect your retirement savings.

Achieve Your Retirement Goals

Get personalized advice to meet your retirement goals. Book your call with Destiny Capital now.