Trade Winds – An Update on The Trump Administration’s Trade Policies

by Tim Doyle, CFP®, MBA

After the stock market closed on Wednesday April 2nd, President Donald Trump took to the stage in the Rose Garden at the White House to further outline his administration’s policies on trade. Since inauguration day, the Trump administration has been attempting to utilize trade policy as a lever to impact a variety of domestic agendas from immigration to drugs to national security. Furthermore, the Trump administration has espoused the notion that the United States is being treated unfairly and taken advantage of by global trade partners. Therefore, President Trump promised ‘reciprocal’ tariffs that would, he claims, balance the scales when it comes to America’s ability to compete on the global stage.

For corporations, foreign governments, consumers and investors, there has been a tremendous amount of uncertainty around the size and scope of these ‘retaliatory’ tariffs. The conventional wisdom was that, after April 2nd, at least economists and investors will know what they’re dealing with and can begin to piece together what any new tariffs may mean for the global economy and, subsequently, financial markets.

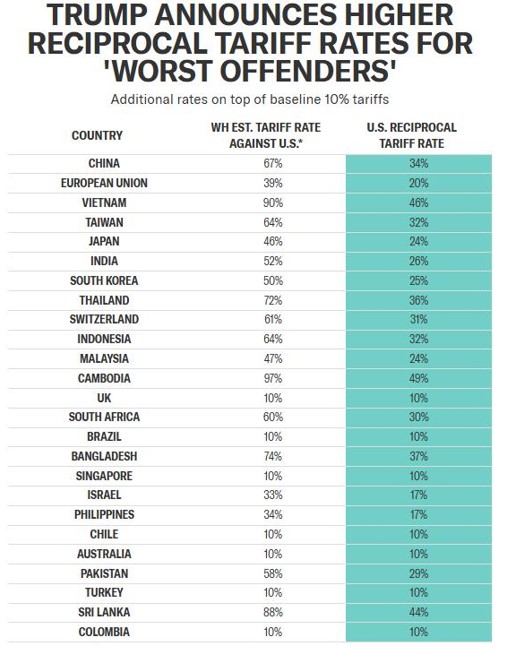

As he spoke in the Rose Garden, Donald Trump announced a new 10% universal tariff on all goods imported into the United States. In most instances, this announcement alone would garner headlines across the globe. However, President Trump then held aloft a board detailing 25 ‘worst offender’ countries along with steep new tariffs for these countries that will go into effect on April 9th at midnight. The list of these countries along with their new tariff rate can be seen in the chart below.

I have to admit, when I first saw the board held aloft by Donald Trump, I did a quick double take. I even did a screen capture on my monitor so I could zoom in on the numbers. Based on what I know about effective tariff rates across the globe, the numbers left me confused. As it turns out, I wasn’t the only one puzzled by what I was seeing, and many investors and economists left the Trump administration’s new tariff event with just as many questions as answers.

This continued uncertainty was immediately evident in after-hours trading on April 2nd as the S&P 500 steeply fell -3% as President Trump was speaking. After the morning bell, the S&P 500 then continued its descent and ended up down -4.84% for the day on Thursday, April 3rd. In fact, nearly all key indexes and assets, except bonds, closed the day sharply down as you can see detailed below.

April 3, 2025 Performance Numbers

S&P 500 Index: -4.84%

Nasdaq: -5.97%

Dow Jones Industrial Average: -3.98%

Russell 2000 Index (Small Caps): -6.59%

All Country World Index Ex U.S.: -2.03%

US Bloomberg Aggregate Bond Index: +0.53%

Crude Oil: -7.13%

Gold: -0.85%

Source: YCharts

This market reaction would indicate that the Trump Administration’s tariffs are even more severe than initially estimated. Now that new tariffs have been announced, the question then becomes “where do we go from here?” So, throughout the rest of this letter, I’ll attempt to outline what might come next in three key areas – The Global Reaction, Fiscal Policy, and the Fed’s Response.

The Global Reaction

I’d wager that many global leaders, particularly those on the ‘worst offenders’ list, were quite taken aback as President Trump revealed the new tariff rates. After all, nobody except the Trump administration’s inner circle truly knew what their definition of ‘reciprocal’ might entail. It turns out that this definition is quite broad.

While I don’t want to go down too many rabbit holes, I think it’s important to detail how the Trump administration calculated the ‘Tariff Rate Against the U.S.A’, as it could directly impact the global response in the coming days. We’ll use South Korea as our example, as South Korea was listed as a ‘worst offender’ with a 50% ‘Tariff Against the U.S.A.’ which, subsequently, results in a new 25% tariff on South Korean imports.

The Trump administration’s method for calculating new tariff rates was dependent on one key factor – whether or not the U.S. had a trade deficit with a particular country. A trade deficit occurs when the U.S. imports more from a country than it exports to that country. Apparently, the view of the Trump administration is that a trade deficit is the sum result of all unfair trade policies implemented by that country over time.

In the case of South Korea, the math is quite simple. The U.S. imports roughly $131.5 billion from South Korea and exports $65.5 billion to South Korea. This results in a trade deficit of $66 billion. To calculate the ‘Tariff Against the U.S.A”, you divide the current trade deficit by the total imports of that country. So, $66 billion / $131.5 billion = 50%. Cut 50% in half and you have your new tariff rate of 25% applied to all South Korean imports as of April 9th.

If these steep new tariffs are intended to be an opening salvo in trade negotiations between the U.S. and trade partners, there may be very little a country like South Korea can adjust to meet U.S. demands. You see, in 2012, the U.S. and South Korea signed the United States-Korea Free Trade Agreement (KORUS FTA). This trade agreement essentially eliminated tariffs between the two countries, and the effective tariff rate on U.S. imports into South Korea is approximately 0.79%.

Therefore, since South Korea does not implement any meaningful tariffs on U.S. goods, they must come up with some other form of concession during any negotiations. After all, a small country like this cannot simply have their corporations and citizens buy $66 billion more of U.S. goods. So, the administration’s unorthodox application of reciprocity could pose some challenges during any future negotiations.

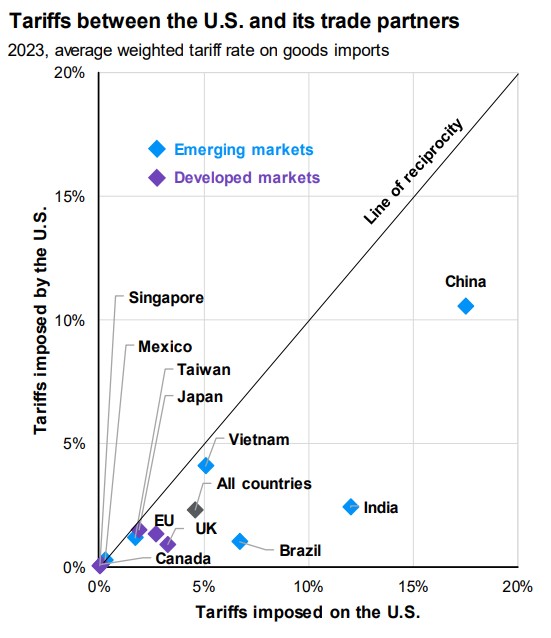

To get a sense for where things stood prior to April 2nd, the chart below helps to illustrate the actual tariff landscape with certain U.S. trade partners. The horizontal axis shows the tariffs imposed by the U.S., and the horizontal axis shows the weighted tariff rate applied to U.S. exports.

As you can see, in terms of actual tariffs (not trade deficits), the worst offenders are countries like China, India, and even Vietnam. In the case of Vietnam, they impose roughly 5% tariffs on U.S. exports while the U.S. only implements a 4% tariff on Vietnamese imports. So, the relationship isn’t entirely reciprocal. However, this is a far cry from what we see on ‘worst offenders’ list where Vietnam is shown to have a 90% ‘Tariff Rate Against the U.S.A.’ Instead, this 90% ‘tariff’ is entirely derived from the trade deficit calculation because the current trade deficit between the U.S. and Vietnam is $123.5 billion, and total imports from Vietnam are $136.6 billion. So, a $123.5 billion deficit divided by $136.6 billion in total imports equates to a 90% ‘Tariff Applied to the U.S.A.’

Ultimately, for some countries, it may take some time to digest these figures and formulate a strategy to respond to the Trump administration’s new trade policies. For others, like China, we are already starting to hear of retaliatory tariffs. In the case of China, they are imposing 34% new tariffs on all products imported from the United States.

You can be certain that there will be domestic political pressure for global leaders to respond to the U.S. in-kind. However, as the most powerful economy in the world, the U.S. remains in a position of strength and global leaders recognize that tit-for-tat tariffs will likely hurt their own economies more than they may hurt the United States. As such, we are hoping for a measured initial response and time for additional negotiations.

Fiscal Policy

I expect the GOP to move aggressively to change the narrative from trade to tax cuts, which could potentially add significant stimulus to the U.S. economy. Yes, we could get a permanent extension of the Tax Cuts and Jobs Act, but we could also see corporate tax rates pushed lower, and there could be added features related to SALT and even the taxation of Social Security, tips, overtime and more. Given the harsh reaction of financial markets, the Trump administration may wish to include as many fiscal ‘carrots’ as possible to boost consumer and investor sentiment.

Also on the table could be a DOGE dividend paid to U.S. households, which could certainly provide some juice to the domestic economy. While tax cuts may impact some Americans more than others, a stimulus check of $3,000 or $5,000 impacts all recipients equally. Stimulus was effective in 2020 as the COVID-19 pandemic pumped the brakes on the global economy, and similar stimulus checks could help the U.S. economy bridge some of the short-term gap as the economy adjusts to this new normal. To be clear, I am not advocating for a DOGE dividend, but believe that it will be an option on the table in the weeks and months ahead.

Furthermore, if fallout continues and pressure builds on lawmakers, we could see Congress act to limit the President’s ability to unilaterally impose tariffs through emergency measures. While this would be unlikely in the current environment, we’ve recently seen a handful of Republican senators join with Democrats to vote on limiting the President’s ability to impose tariffs on Canada. While that action likely will not pass (or even see a vote) in Congress, those dynamics could change if certain lawmakers in contested swing states receive more and more pressure from their constituents to act. Again, this scenario is not likely, but exists in the realm of possibility. After all, if politicians value anything, it’s keeping their jobs, and midterm elections could weigh on the minds of many lawmakers if these trade policies lead to slower growth and higher unemployment.

The Fed’s Response

The Trump administration’s new trade policies appear to put the Fed in a bit of a pickle. Given the persistence of inflation in recent months, the Fed has been on a very patient path as it relates to interest rate policy. In an ideal world, the Fed would like to lower rates gradually over time in order to maintain a strong labor market while keeping inflation on a downward, albeit very slow, trajectory. However, the new trade policies of the Trump administration may force the Fed’s hand in the coming weeks and months.

Tariffs are inherently inflationary as the added costs of tariffs tend to be passed-on to the consumer, which puts upward pressure on aggregate prices. In the short-term, these tariffs could also lead to declining economic growth and, subsequently, a weaker labor market if corporations are forced to layoff workers to maintain profitability levels. Therefore, the Trump trade policies could directly impact the Fed’s two mandates around stable prices and full employment.

When it comes to choosing which mandate to prioritize in the months ahead, I believe the Fed will opt to boost economic growth and, hopefully, keep unemployment from rising. This should equate to several rate cuts between now and year-end. Right now, markets are pricing-in a rate cut of either 0.25% or 0.50% during the Fed’s June 18th meeting, and investors believe that rates could fall by 1.00% or more by year-end.

Lower rates and accommodative Fed policy, particularly if coupled with fiscal stimulus, could certainly add some fuel to the U.S. economy in the weeks and months ahead. Investors will be watching any-and-all Fed commentary very closely to gauge the direction of monetary policy and what impact it might have on financial markets.

Maintaining Perspective

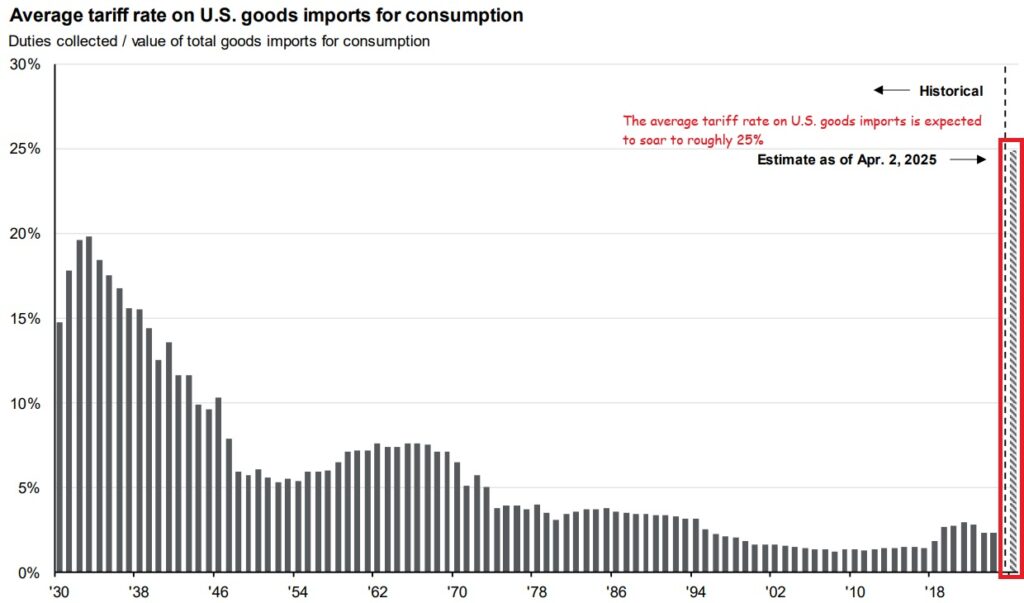

If you are concerned about the economy and financial markets, that is completely justifiable and understandable. The past two days have been quite jarring for the economy and stock market alike. In fact, the current environment reminds me a bit of the onset of the COVID-19 pandemic back in early 2020. As was the case in 2020, there has been a sudden shock that impacts nearly every facet of the global economy. Ground rules for the economy have literally changed overnight with the average tariff rate on imported goods rising from roughly 2% to 25% – figures that exceed levels last seen in the 1930’s, as you can see below.

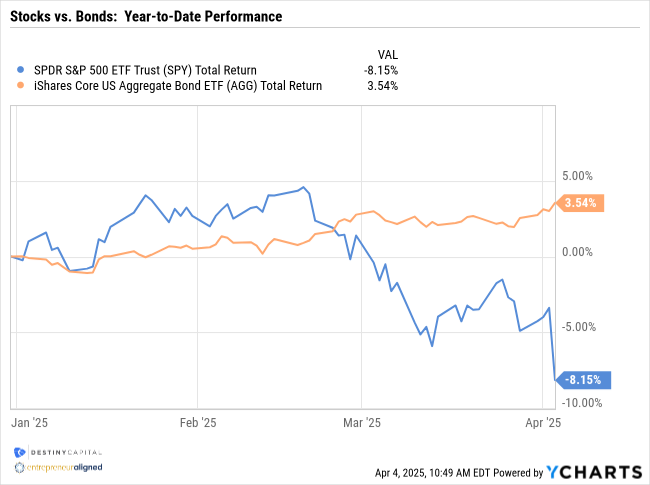

This has forced many investors into a reactive posture, which can often lead to poor decisions. Instead, at Destiny Capital, we tend to focus on proactively constructing portfolios that can potentially buffer against periods of elevated volatility. The benefits of diversification and mindful portfolio construction can be seen in the chart below that shows the performance of the S&P 500 Index on a year-to-date basis alongside the Bloomberg US Aggregate Bond Index. As you can see, bonds are behaving as intended by moving higher as the stock market sells-off. So, for investors who are diversified across fixed income, they are not feeling the full brunt of day-to-day volatility.

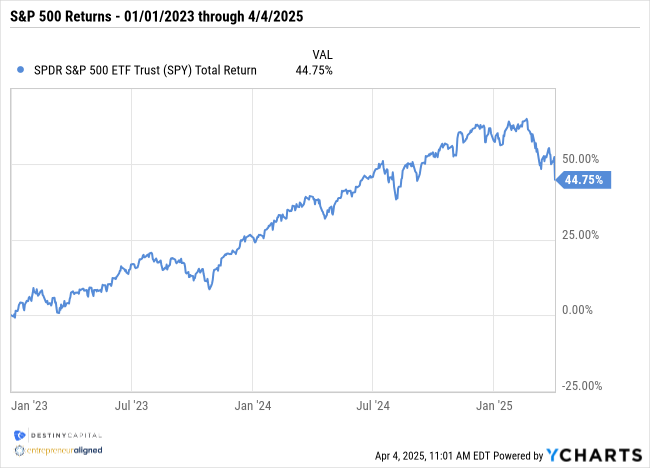

As long-term investors, it’s also important to view the stock market through a longer-term lens. For example, the chart below shows returns for the S&P 500 since the beginning of 2023 and, as you can see, stocks have soared in recent years and this latest pullback, while far from enjoyable, has not yet erased all progress from recent years.

As we’ve communicated in recent blogs and webinars, it can be very tempting to chase returns or sit on the sidelines in cash when volatility strikes. However, these reactions can be fraught because markets move with extreme rapidity.

As they have in recent days, markets take bad news and immediately price-in a worst case scenario within hours. Conversely, when the worst fails to materialize and/or when good economic news is released, markets can often move sharply higher. In fact, the best days in the stock market tend to occur within 2 weeks of the worst days. It’s impossible to predict when the stock market will move higher or lower, so it’s crucial for investors to remain disciplined, diversified, and stick with their game plan, particularly when markets experience an unexpected selloff.

Clearly, new developments are emerging rapidly and, as we’ve indicated throughout this letter, we will be watching closely to gauge the global response to tariffs, the GOP’s plan around fiscal stimulus, and any shifts in the Fed’s policies around interest rates. As always, we will continue to communicate with you as this situation evolves and, in the meantime, please do not hesitate to contact your Strategist or Coordinator with any questions.

Important note and disclosure: This article is intended to be informational in nature; it should not be used as the basis for investment decisions. You should seek the advice of an investment professional who understands your particular situation before making any decisions. Investments are subject to risks, including loss of principal. Past returns are not indicative of future results. Advisory services offered through Destiny Capital Corporation, an Investment Adviser registered with the U.S. Securities & Exchange Commission.

2024 YCharts, Inc. All Rights Reserved. YCharts, Inc. (“YCharts’) is not registered with the U.S. Securities and Exchange Commission (or with the securities regulatory authority or body of any state or any other jurisdiction) as an investment adviser, broker-dealer or in any other capacity, and does not purport to provide investment advice or make investment recommendations. This report has been generated using data manually input by the creator of this report combined with data and calculations from YCharts.com and is intended solely to assist you or your investment or other adviser(s) in conducting investment research. You should not construe this report as an offer to buy or sell, as a solicitation of an offer to buy or see, or as a recommendation to buy, sell, hold or trade, any security or other financial instrument. THE IMPORTANT DISCLOSURES FOUND AT THE END OF THIS REPORT (WHICH INCLUDE DEFINITIONS OF CERTAIN TERMS USED IN THIS REPORT) ARE AN INTEGRAL PART OF THIS REPORT AND MUST BE READ IN CONJUNCTION WITH YOUR REVIEW OF THIS REPORT. Disclosure – YCharts

Share this

Stay Ahead with Smart Investments

Learn how to invest wisely and minimize risks to protect your retirement savings.

Achieve Your Retirement Goals

Get personalized advice to meet your retirement goals. Book your call with Destiny Capital now.