CIO Mailbag: The Investment Implications of War with Iran

by Tim Doyle, Chief Investment Officer, CFP®, MBA

The first quarter of 2026 has yet to conclude, and investors are already starting to feel like they are on the wrong end of a combination from boxing great Floyd Mayweather Jr. The first jab came in early January when the United States carried out Operation Absolute Resolve that led to the capture of Venezuelan leader Nicolas Maduro and his wife. Then a quick right hook followed when the U.S. Supreme Court ruled that the Trump administration’s sweeping global tariffs are unlawful under the International Emergency Economic Powers Act (IEEPA). Finally, a powerful uppercut landed in recent days with the United States and Israel carrying out large-scale air and naval operations against Iran and their regional proxies which has resulted in the deaths of many Iranian leaders including Supreme Leader Ayatollah Ali Khamenei.

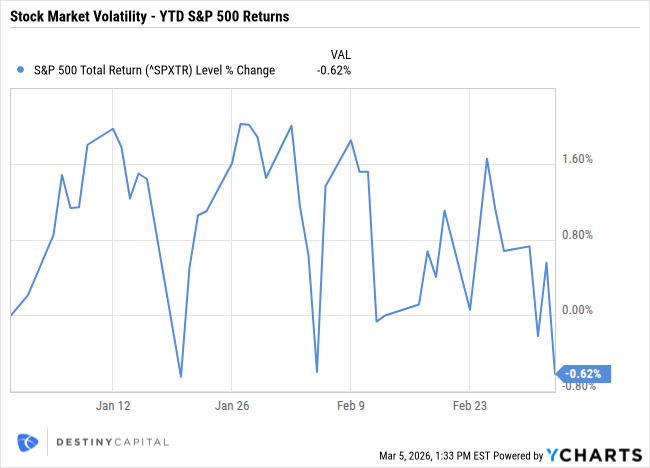

Each of these events on their own would be enough to generate considerable uncertainty across global financial markets. Combine these events into a two month window, and investors are starting to feel a little punch drunk and wary of when the next blow might land. As you can imagine, the situation in Iran is evolving by the minute and markets have been extremely reactive to headlines. This is evident in the chart below that shows the year-to-date returns for the S&P 500 index. In the industry, we refer to this type of advance-and-decline market activity as ‘whipsawing’, which is a hallmark of uncertainty and volatility.

As long-term investors, it’s important not to get swept-up in the daily and weekly fluctuations in the stock market. However, the unpredictability of war can make it difficult to ignore the short-term implications of military action, particularly if it becomes apparent that military action is going to be prolonged.

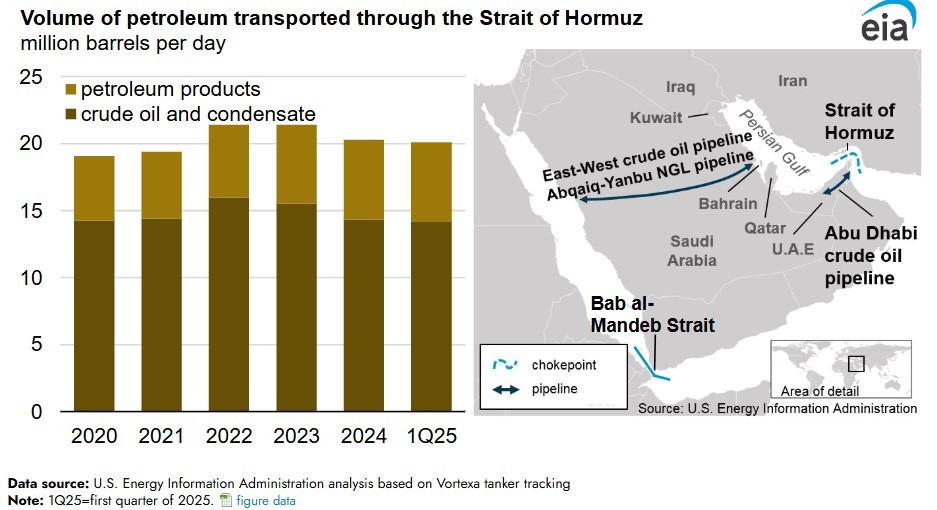

When it comes to the near-term impact for financial markets and the economy overall, it’s impossible to talk about war in the Middle East and not consider the impact on a vital commodity like oil. Iran isn’t necessarily a major player when it comes to oil exports these days, as the country only accounts for roughly 4% of global oil supply. However, geographically speaking, Iran is a major player when it comes to the transportation of oil given the crucial importance of the Strait of Hormuz which is a choke point in the Persian Gulf that runs between southern Iran and northern Oman. As you can see in the graph below, roughly 20 million barrels of petroleum are moved through the Strait of Hormuz each day, which represents about 20% of the global oil supply.

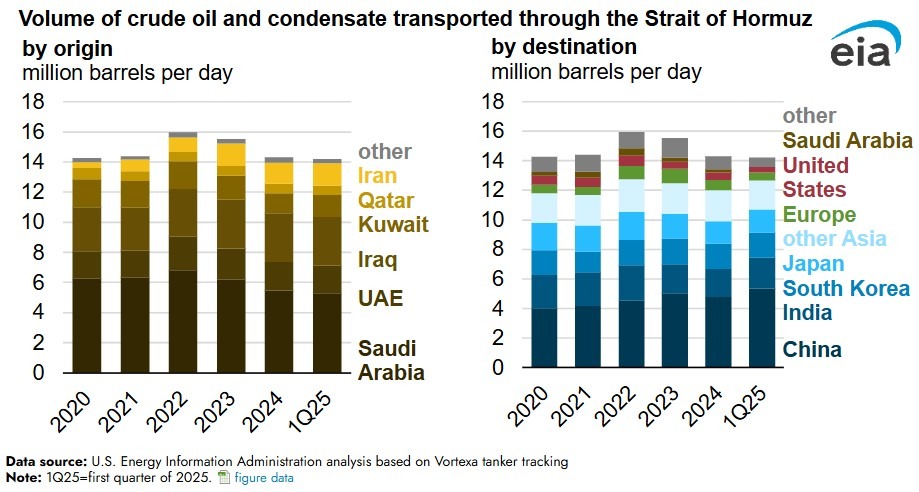

As of this writing, major shipping and tanker operations have suspended transit through the Strait of Hormuz due to the war with Iran. However, when it comes to the immediate impact of this closure on the U.S. economy, it’s important to remember that the United States is a net exporter of oil and is far less reliant on Middle Eastern oil imports than it was decades ago. The chart below helps to illustrate this by showing the sources and recipients of oil transported through the Strait of Hormuz each day. As you can see on the right side of this chart, countries like China and India are far more reliant on oil from the Middle East than the United States.

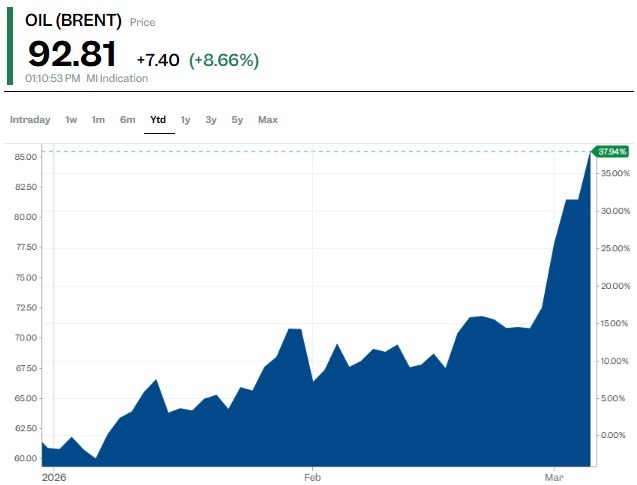

Having said that, the U.S. economy is not immune to broader movements in commodity markets, and the war with Iran and the subsequent closure of the Strait of Hormuz is causing a short-term supply shock that has caused the price of oil to skyrocket above $92 per barrel as-of this writing.

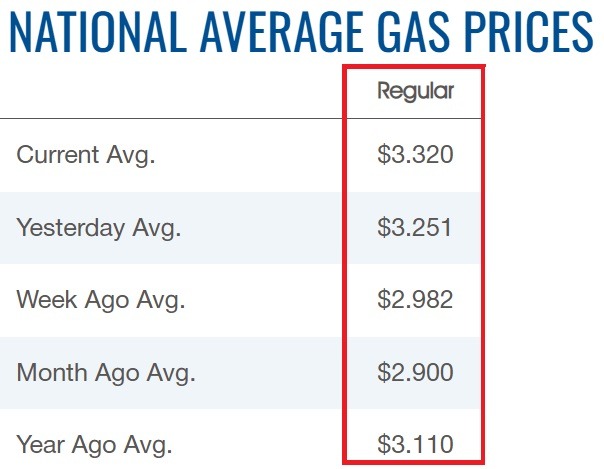

Furthermore, prices at the pump in the U.S. have surged nearly $0.34 cents per gallon in a matter of days as you can see in the table below from AAA that shows average national prices for regular unleaded gasoline.

Higher energy prices could impact the broader U.S. economy in a number of ways. For example, if higher energy prices are persistent, this would undoubtedly cause inflation to surge in the months ahead. Core PCE (the Fed’s preferred measure of inflation) is already at 3.0%, so if we see core inflation move to 3.5% or higher, it could be challenging for the Fed’s new leadership to justify additional rate cuts. Given these dynamics and the uncertainty around the war in Iran, investors are now predicting just one 0.25% rate cut between now and year-end.

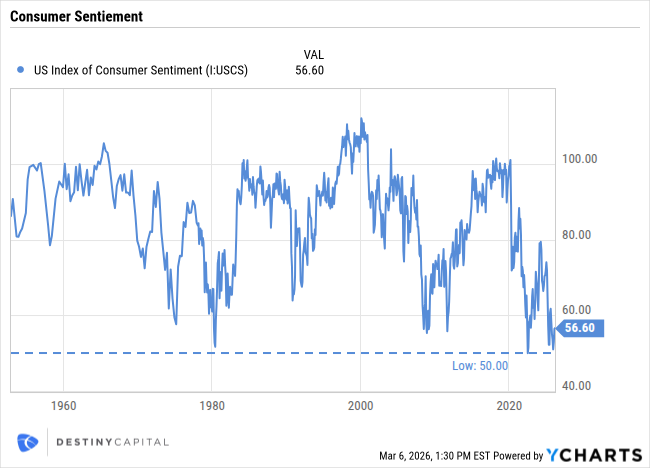

Furthermore, if the past few years have taught us anything, it’s that inflation can be incredibly detrimental to consumer mindset. As aggregate prices rise, we tend to see U.S. consumers grow increasingly pessimistic about the economy, and this can be seen in the chart below that tracks consumer sentiment since the early 1950’s. As you can see, consumer sentiment fell to an all-time low in June of 2022 as inflation surged over 9%, and consumer sentiment has declined once again in recent months as shelter, food and utility prices have remained stubbornly high.

Fortunately for the U.S. economy, a pessimistic mindset among consumers hasn’t negatively impacted consumer behavior in recent years, as spending has remained strong. Additionally, consumers are expected to receive a shot in the arm in the coming weeks in the form of larger tax refunds due to the Trump administration’s OBBB tax bill. The average tax refund is estimated to jump from roughly $3,200 in 2025 to nearly $4,100 in 2026, and this is expected to boost consumer spending in the coming months and provide some tailwinds for GDP growth in the coming quarters.As it stands now, the economic impact of the war with Iran is almost entirely dependent on the length and severity of the conflict. Markets are currently pricing-in a three to four week disruption of petroleum transport through the Strait of Hormuz. If the timeline extends beyond that, experts believe that oil prices could surge well above $100 per barrel in the coming weeks and months.

Fortunately, the United States holds virtually all of the cards when it comes to dictating the timeframe of this conflict. When considering the ‘end-game’ in Iran, the Trump administration has been somewhat vague in outlining their justification for the conflict and what victory might look like. This gives the administration a number of off-ramps in the days and weeks ahead to declare ‘mission accomplished’ which could allow shipping through the Strait of Hormuz to recommence.

After all, many of the risks around energy prices and inflation exist particularly if this conflict is prolonged and there is a lengthy disruption to petroleum transport in the Middle East. Given that mid-term elections are on the horizon, politicians have a vested interest in ensuring that this conflict gets resolved in a timely fashion without a significant, negative economic impact in the United States.

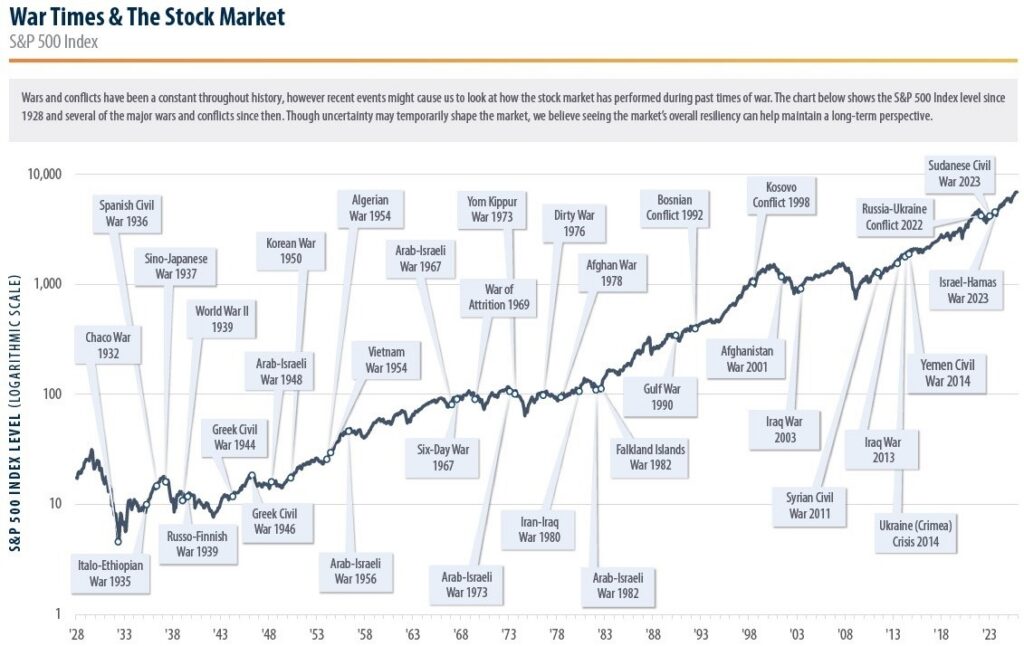

It’s an unfortunate fact that investors have endured many geopolitical conflicts over the decades. The chart below helps to demonstrate this by illustrating the upward trajectory of the S&P 500 despite consistent geopolitical disruption. This serves as a reassuring reminder that the stock market has remained incredibly resilient over time and investors have been rewarded despite periods of elevated risk and volatility like we see today.

Of course, the military engagement with Iran continues to evolve and updates are being delivered by the minute. We will continue to monitor the situation closely and will be sure to communicate any developments that may have meaningful implications for markets or client portfolios. In the meantime, our thoughts remain with the men and women in uniform who are serving our country, and we hope for a peaceful resolution to this conflict in the days ahead.

Important note and disclosure: This article is intended to be informational in nature; it should not be used as the basis for investment decisions. You should seek the advice of an investment professional who understands your particular situation before making any decisions. Investments are subject to risks, including loss of principal. Past returns are not indicative of future results. Advisory services offered through Destiny Capital Corporation, an Investment Adviser registered with the U.S. Securities & Exchange Commission.2024 YCharts, Inc. All Rights Reserved. YCharts, Inc. (“YCharts’) is not registered with the U.S. Securities and Exchange Commission (or with the securities regulatory authority or body of any state or any other jurisdiction) as an investment adviser, broker-dealer or in any other capacity, and does not purport to provide investment advice or make investment recommendations. This report has been generated using data manually input by the creator of this report combined with data and calculations from YCharts.com and is intended solely to assist you or your investment or other adviser(s) in conducting investment research. You should not construe this report as an offer to buy or sell, as a solicitation of an offer to buy or see, or as a recommendation to buy, sell, hold or trade, any security or other financial instrument. THE IMPORTANT DISCLOSURES FOUND AT THE END OF THIS REPORT (WHICH INCLUDE DEFINITIONS OF CERTAIN TERMS USED IN THIS REPORT) ARE AN INTEGRAL PART OF THIS REPORT AND MUST BE READ IN CONJUNCTION WITH YOUR REVIEW OF THIS REPORT. Disclosure – YCharts

Share this

Stay Ahead with Smart Investments

Learn how to invest wisely and minimize risks to protect your retirement savings.

Achieve Your Retirement Goals

Get personalized advice to meet your retirement goals. Book your call with Destiny Capital now.